Buying or renting in Paris in 2026 remains one of the most delicate wealth management decisions. The answer is never one-size-fits-all: it depends on your personal situation, your life plans, and the state of the Parisian real estate market. Before committing to a twenty-five-year mortgage or signing a lease, it is best to understand the forces at play and evaluate the decision based on total cost rather than gut feeling.

The Parisian real estate market in 2026: where do we stand?

Contrary to a still widespread belief, Parisian prices are no longer falling. After several years of correction between 2020 and 2025, the market has entered a phase of stabilization, followed by a moderate recovery: according to leading market observatories, prices are now rising by around +3% to +5% year-on-year. The average price currently stands between €9,800 and €11,000 per square meter, with dramatic gaps from one arrondissement to another: around €8,800/sqm in the 20th compared to over €16,000/sqm in the 6th.

On the rental side, tension remains high. Demand significantly outstrips supply, available properties are scarce, and rent control, in effect since 2023, caps rent levels by neighborhood and property type. Added to this, since January 1st, 2026, tougher rules on the DPE (Energy Performance Certificate) are progressively removing the most energy-inefficient homes from the market.

Finally, the cost of credit impacts any purchase calculation: interest rates are hovering around 3.5% to 4% over 25 years, a far cry from the 1% seen a few years ago. This factor radically changes the profitability of an acquisition financed through a mortgage.

Buying in Paris: when does it become profitable?

The decisive criterion is the length of occupancy. In Paris, buying only becomes truly worthwhile if you plan to stay for the long term. The break-even threshold compared to renting is generally between 7 and 12 years. In the most upscale arrondissements, where the price-to-rent ratio is very high, this threshold often exceeds 15 years, with some studies even placing it beyond 20 years.

Below this timeframe, upfront costs are too heavy to be amortized: notary fees (7% to 8% for existing properties), agency fees, loan processing, and guarantee fees. On top of that, banks now require a solid personal contribution (down payment), usually between 10% and 20% of the purchase price—representing several years of savings for a Parisian property.

In which cases is buying the obvious choice?

Acquisition becomes the clear choice in several scenarios:

- A stable life plan, with an intended ownership horizon of more than 15 years;

- A solid down payment, which reduces the borrowed capital and the cost of interest;

- A wealth-building approach: gradually accumulating a transmissible asset;

- Tax advantages specific to primary residences, foremost among which is the total capital gains tax exemption upon resale, regardless of how long the property was held;

- Access to the zero-interest loan (PTZ), subject to income ceilings.

Renting in Paris: a wealth management strategy in its own right

Renting is too often perceived as "throwing money away." This is a misconception that deserves nuance, especially in Paris. Renting, first and foremost, preserves valuable freedom of mobility when your professional or family future is uncertain: relocations, career changes, expatriation, or an expanding family.

It is also an opportunity to adopt an alternative wealth management approach: investing differential savings rather than locking capital into brick and mortar. Placed in life insurance (assurance-vie), SCPIs (real estate investment trusts), ETFs, or private equity vehicles, the difference between a rent payment and a monthly mortgage installment can generate, over time, a return higher than the mere capital appreciation of a Parisian property. Furthermore, remaining a tenant limits exposure to the Real Estate Wealth Tax (IFI).

Finally, beware of misleading comparisons. Pitting a rent payment against a monthly mortgage installment distorts the analysis, as property ownership comes with regular expenses that are often underestimated: property tax, sometimes high co-ownership charges, repairs, and property maintenance. The right reflex is to think in terms of total cost of ownership.

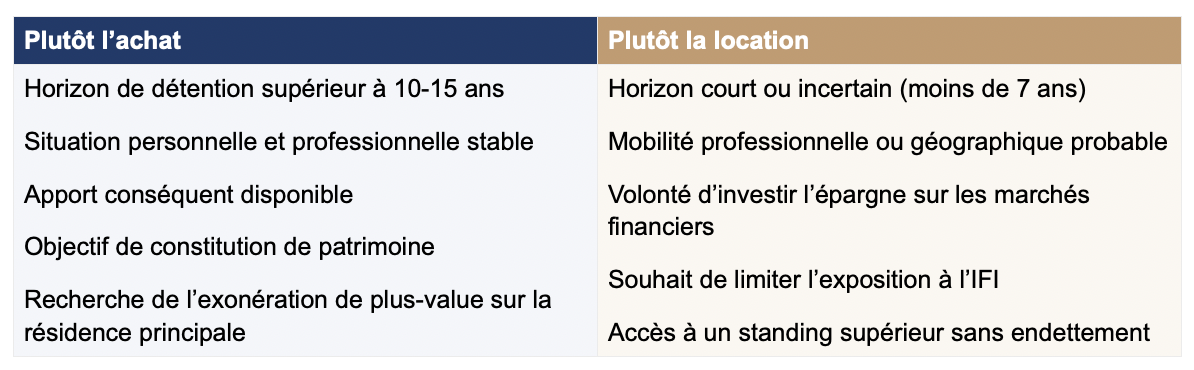

Buying or renting in Paris: how to decide?

There is no single correct answer in absolute terms, but rather profiles to which each option is best suited. This table summarizes the major trends.

Frequently Asked Questions

After how many years does a purchase become profitable in Paris?

On average between 7 and 12 years, depending on the property price, the neighborhood, and financing conditions. In premium arrondissements, this threshold frequently exceeds 15 years. Below 7 years, renting almost always remains more advantageous, as upfront entry costs are not amortized.

What is the average price per square meter in Paris in 2026?

Roughly €9,800 to €11,000/sqm on average, with a range stretching from nearly €8,800/sqm in Eastern arrondissements to over €16,000/sqm in the most sought-after areas of the Left Bank and the West. After several years of decline, prices have turned upward again in 2026.

Is renting in Paris really throwing money away?

No, provided that you actively invest the savings generated. A disciplined tenant who invests the monthly difference between their rent and the real cost of a property acquisition can, in the long run, build up equity comparable to, or even greater than, that of a homeowner—all while maintaining their freedom.

Is the purchase of a primary residence subject to the IFI?

The primary residence is included in the IFI tax base, after a 30% deduction on its value. Remaining a tenant prevents this tax base from expanding, which can be an important factor in the decision-making process for households concerned by this tax. A personalized analysis is essential.

Conclusion: make the right wealth management choice with Forward Us

Ultimately, there is no universal answer. Buying in Paris in 2026 remains a long-term choice, offering the peace of mind of building and transferring wealth. Renting, conversely, offers a freedom and an investment capacity that are still widely underestimated. In any case, it is a personalized approach—backed by numbers, tax analysis, and asset strategy—that must guide your decision.

At Forward Us, we support you in identifying the best solution for your situation, drawing on the expertise of our wealth management partner, VIA Gestion de Patrimoine. Let’s discuss your real estate and wealth-building projects.

Book an appointment: calendly.com/w-benberkane/60min